Awardco and Rain: Recognition meets financial health

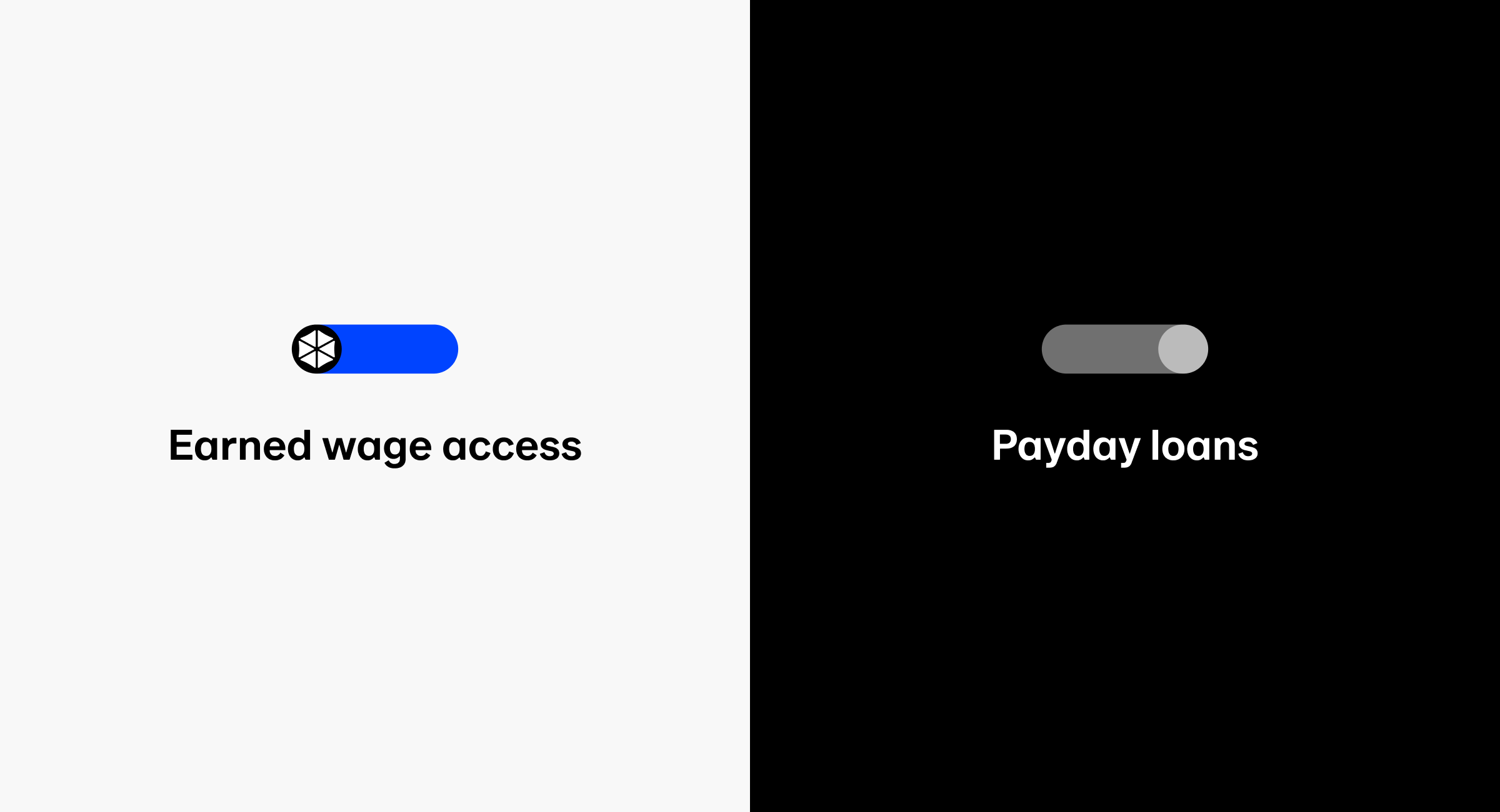

Rain and Awardco are partnering to give employers a complete employee experience, where workers feel valued for their work and supported when finances get tight.

Product updates, insights and behind the scenes directly from the Rain team.

No matches found

© 2026 Rain Technologies Inc.